Chatsworth Securities LLC is pleased to announce the latest strategic partnership with OPER Pay, (OPER, LLC DBA OrderEx), a unique payment engine designed to make mobile payments easier for the customer. OrderEx, is an all-in-one digital ordering and mobile payment platform that will take a brand or merchant’s retail operations to the next level.

“OrderEx’s is a very advanced QR payment platform offering customers a seamless experience at the retail level. It places a lot of power and freedom in the user’s hand without the need of downloading an app” said Marcus Magarian, Managing Director at Chatsworth. “Chatsworth Securities has significant experience in digital payments and the data analytics space. The analytical first-party data alone could unlock actionable insights for brands to improve the customer’s in-store experience and help brands drive more revenue”, continued Marcus. Chatsworth will provide the company with expanded access to capital, improvement in business metrics, and potential business opportunities.

The OrderEx platform enables the seamless integration of payment processing and technology solutions across a variety of markets at brick-and-mortar locations. It gives the user a suite of tools to save time and safely serve more customers. It tackles tedious tasks so staff can spend more time with guests. With interactive menus, mobile ordering and payment, customer rewards, and on-demand server engagement and communication, restaurants can ensure high performance and high-touch service – even during the busiest rush.

OPER was founded by Dave Laiderman, CEO who began developing payments technology in college and has been addressing the challenges restaurants face for nearly 20-years. “Integrate OrderEx with your current POS system or payment provider in as little as two hours. Customers browse and order from their mobile phone; and, when they are done, they pay directly from their mobile phone,” he said.

Chatsworth is an investment banking firm that also provides consulting and advisory services. “We not only provide M&A and raise capital for clients but help clients with business challenges and opportunities” stated Ralph DiFiore, Senior Managing Director of Chatsworth. He added, “Given the challenges businesses face today we are all about helping our clients improve business metrics such as revenues, profits, and EBITDA. One way to improve these metrics is to unlock the revenue potential of their “on-premise” data which is extremely valuable to major consumer goods conglomerates and QSR groups, for example”.

OPER Payments Technology Demo Video

5Thru & Chatsworth seek to Digitally Transform the Drive-Thru Experience.

Chatsworth Securities LLC is pleased to announce the latest strategic partnership with 5Thru, an innovative drive-through payments platform. 5Thru’s technology seeks to digitally transform the drive-thru experience by simplifying and personalizing it—allowing for a faster, frictionless experience. The partnership will focus on business development and strategic advisory to help boost 5Thru’s market share to digitally transform the drive-thru market, such as in the: QSR/fast-food, pharmaceuticals, banking, etc. sectors.

5thru provides the missing link for in-vehicle customer engagement by reducing bottleneck pain points in the drive-thru customer journey. Using an innovative Customer Profile builder and identification technology tied to order history, AI recommender, and automatic payment, there’s a solution that adapts to both the consumer and businesses’ changing perceptions of convenience. 5thru offers a range of drive-thru retailers a deeper way to engage, serve and speed service with efficiency, accuracy, and automation.

“We are personalizing the drive-thru experience and improving the speed of service. 5Thru utilizes image recognition technology to offer a secure contactless payment option, reducing the average wait times by 22 seconds, resulting in more traffic, more revenue, and increased customer loyalty,” said James Clifford CEO of 5Thru. 5Thru was founded by Daniel McCann, who has founded several successful technology start-ups throughout his career and has developed tremendous experience in the payments and image recognition technology space.

“Today, most restaurant groups have digitally transformed and adopted digital payments technology. However, over 80% of restaurants are turning to other technology, such as: online ordering, reservation, digital menu, inventory apps, restaurant analytics, etc. more than ever to help them run their business successfully and efficiently. This is no different at the drive-thru”, stated Marcus Magarian, Managing Director at Chatsworth Securities LLC. “Chatsworth Securities has deep industry expertise in the payments space, and we believe that 5thru’s technology improves the drive-through experience for the customer” continued Marcus. We are looking forward to providing our niche knowledge and experience in the digital hospitality space through this partnership.

Demo Video of How 5thru works?

About 5Thru

5Thru Customer Profile builder provides the missing link for in-vehicle drive-thru engagement. Using innovative AI, our Customer Profile Builder technology, tied to order history provides a drive-thru solution that adapts to both the consumer and businesses’ changing perceptions of convenience.

The financial technology boom observed over the past few years has significantly impacted Latin America’s fintech ecosystems. As discussed in the Payments in the Middle East article, rapid growth in smartphone and internet adoption is fueling fintech VC and M&A markets in Latin America. Small and medium-sized businesses have increased access to banking and financial services resulting in an abundance of fintech startups in the region.

LatAm Fintech Growth

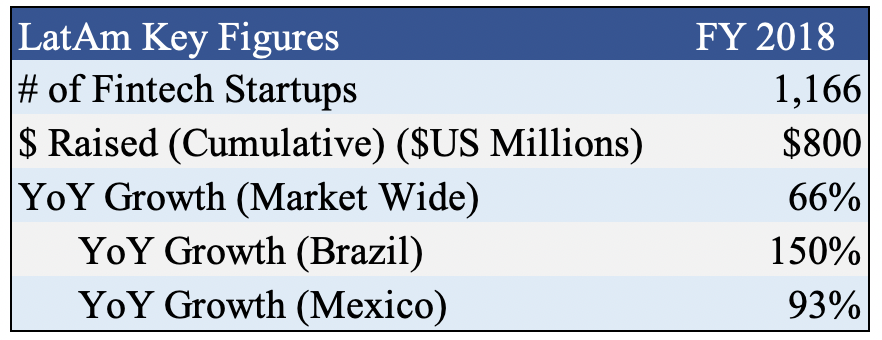

Latin America has experienced exceptional growth in the fintech space since 2018. The below figure details some key figures of the fintech landscape in Latin America in 2018.

Since 2018, the fintech landscape in Latin America has shown continued growth. A catalyst for the growth experienced in the fintech industry in Latin America has been operational changes forced by pandemic life and the increased venture capital interest in the region’s ecosystem. Latin American fintechs secured $481m in funding in Q2 2019, a six-quarter high for the region at the time.[1] This $481m in funding topped both China and India Q2 funding in 2019. The $481m is 69% of the total venture capital raised in LatAm in all of 2018. Furthermore, LatAm-based fintech funding has grown at a 57% CAGR since 2016. South America funding has grown 153% quarter-to-quarter.

Accelerated Growth Continues in the New Decade

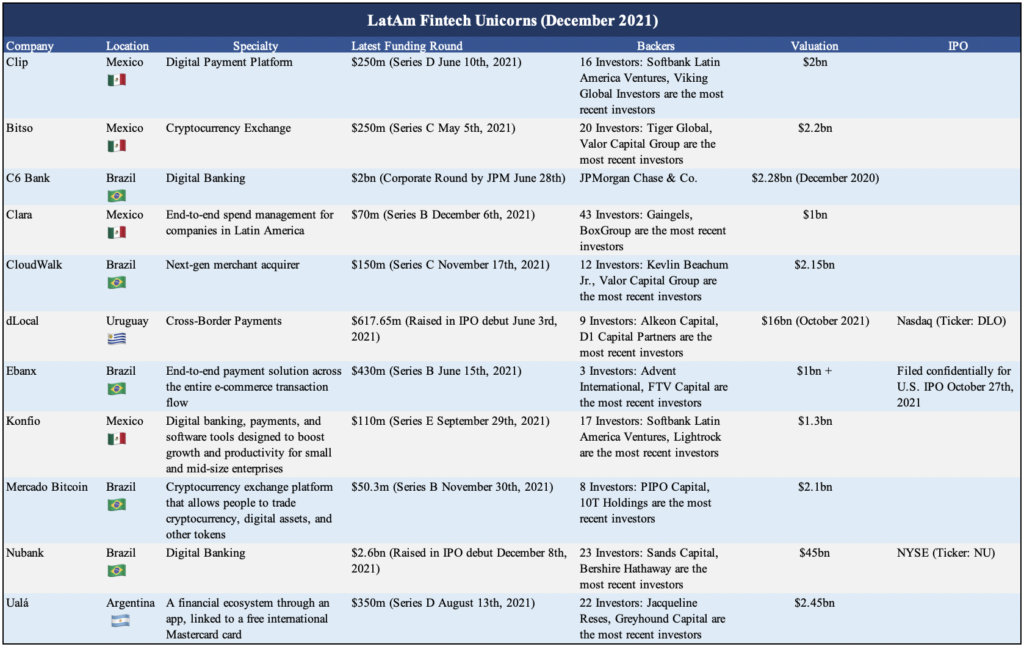

Growth trends of 2018 and 2019 continue, and interest from foreign investors builds. In 2020, VC firms invested $4bn spread over 488 transactions in LatAm startups. Fintechs saw 39% of the total amount invested in their sector. In the first half of 2021, Latin America’s fintech sector raised $7.6bn.[2] Investments increased twelvefold in the second quarter of 2021 compared with the same period of 2020. Five Latin American fintech companies achieved unicorn status in the first half of 2021 – Clip and Bitso in Mexico, dLocal in Uruguay, and C6 and Ebanx in Brazil. By December, eleven Latin American fintech companies achieved unicorn status – making up 52.4% of total unicorn startups in the region. Two firms saw U.S. IPOs in 2021 (Nubank; dLocal) and one more confidentially filed for a U.S. IPO in October 2021 (Ebanx). Uruguay’s dLocal June U.S. IPO minted a new female billionaire cofounder. Bitso achieved the status of Latin America’s first crypto unicorn. In the first nine months of 2021, startup funding is up 174% from all of 2020, with at least 25 M&A deals so far just among startups.[3]

An overview of Latin American fintech unicorns can be seen below:

The Latin American fintech markets are red-hot and are not expected to slow down in the coming months. Major players in private equity and venture capital such as Softbank Group Corp, General Atlantic, and Sequoia Capital have their eyes on the LatAm fintech boom, fueled by the internet boom accelerated by pandemic lockdowns. Shoppers’ necessity to move online and growth in contactless payments to reduce COVID-19 spread has allowed innovators to take advantage of widespread and increasing use of smartphones, wireless networks, and payments cards. Furthermore, the comfortability of digital wallets has increased in the region. As a result, Latin America presents many opportunities for domestic and foreign businesses alike to grow by acquiring innovative LatAm-based firms. M&A can function as a key strategy for firms looking to gain a strategic advantage without developing the competitive edge they are seeking through in-house building and development – which could require a significant amount of time and capital. The current landscape in Latin America presents interesting opportunities for firms with expertise in M&A, private placements, and strategic advisory services to help clients in an exciting emerging financial technology market.

Consistent with the rest of the world, COVID-19 accelerated the adoption of digitized and contactless payments in the Middle East.

Despite 80-90% smartphone penetration in GCC Arab States, Israel, Iran, and other leading markets, the Middle East is still heavily dependent on cash. In the region, only one-third of retail transactions are conducted electronically. Underdeveloped digital-payments infrastructure and services, underbanked consumer and merchant segments, and a cultural preference for cash contributions to lacking digital payments integration.

In spite of this preference for cash, transactions card payments still managed to grow 70% in the year before the pandemic from February 2019 to January 2020. Another indication that sentiment is changing was found in the UAE where consumer digital payments transactions grew more than 9% annually between 2014 and 2019 (compared to Europe’s 4-5%).

Key Growth Statistics

Saudi Arabia’s digital POS transactions doubled over 2020. 90% of survey participants believe more than half of new users will stick to digital solutions adopted during the pandemic.

In McKinsey’s August 2021 survey on payments in the Middle East, more than 80% of respondents believed the growth rate of non-cash payments rose more than 10%. 43% placed the growth rate at over 20%.

With survey respondents favoring marketplaces and specialist fintechs over banks, local acquires, and e-wallets by 33% percent, respectively, SMEs are believed to seek solutions that go beyond pure payments. The growth opportunity resulting from SME preferences led 43% of respondents to believe that more than half of small and medium-sized merchants will start selling online in the next five years consequently resulting in growth in digital payments. In addition, lower merchant discount rates are expected to fuel the transition and adoption of digital payments.

Current Payments Sentiment in the Middle East

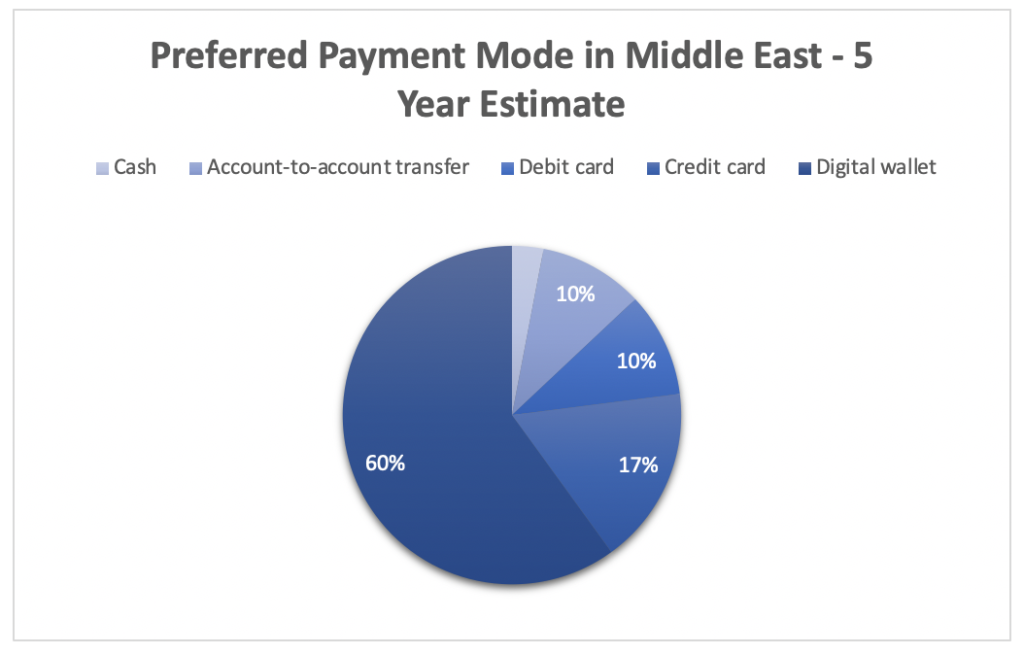

Despite COVID-19’s immediate impact, consumer preferences data supports the continued growth of the digital payments market in the Middle East. 58% of consumers in the Middle East expressed a strong preference for digital payment solutions.[1] Alternatively, only 10% strongly preferred cash. In the next five years, Middle East experts expect digital wallets (e-wallets) to be the most preferred mode of payment. The graph below depicts a five-year estimate of preferred payment methods in the Middle East based on the McKinsey survey mentioned above.

Nonbanks as Market Leaders

Global big-tech companies are expected to dominate consumer digital payments, with telecom company wallets and banks or bank-backed wallets trailing closely behind. In the Middle East, big-tech and telecom companies are favored in payments over incumbent banks due to their competitive advantage in technology expertise and well-established broad reach. These firms are expected to have a leg up in development and a better understanding of consumer preferences.

Telecoms’ success in digital payments.

Saudi Telecom Company’s STC Pay leveraged its strong telecoms presence to scale 4.5 million active customers by November 2020. 55% of mobile subscribers to STC Pay are STC customers. Partnerships with Western Union (raised $200 million at a $1.3 billion valuation) and Mastercard have enabled the company to cater to customer preferences and win market share.

Open Banking

Open Banking regulatory reforms are expected to help shape the future of payments in the Middle East. Open banking requires banks, with the consent of their customers, to share customers’ financial data with other banks or authorized financial services providers. In the Middle East, Bahrain passed regulations to institute open banking rules in 2018, followed by governance and data sharing guidelines in 2020. In early 2022, Saudi Arabia plans to launch open banking. Survey respondents identified regulatory approval for open banking as the leading catalyst for widespread customer adoption of digital payments. Incentivizing the shift from cash to digital payments for customers trailed open banking as a catalyst for digital payment adoption by 7%.

Open banking allows payments to avoid banks in the monetary transactions. 80% of survey respondents believe the implementation of open banking regulations will spark decoupling of savings account balances and payments capabilities. In this open banking environment, customers are expected to favor payment services companies with a better customer experience than banks, which tend to lack user-friendly payments ecosystems. STC Pay and other nonbanks can be expected to continue to thrive and win market share as the payments space transforms with open banking legislation.

Cross-border Ecosystem Developments

Cross-border payments in the Middle East require real-time, reliable digital payment infrastructure. The UAE and Saudi Arabia are home to two of the world’s three largest remittance corridors, processing $78 billion in payments in 2020. The necessity for agreements between countries for real-time settlement and the scaling up of digital money-transfer operators are expected to drive cross-border transactions in the near to mid-term.

Active Cross-Border Transaction Initiatives in the Middle East

Initiative

Who

Description

Project Aber

Saudi Arabia & the UAE

Initiative produced a common digital currency between Saudi Arabia and the UAE

The Buna Payment Platform

Members of the Arab Monetary Fund

Initiative supports multicurrent payments among the members of the Arab Monetary Fund

The AFQ System

Countries in the Gulf Cooperation Council (GCC)

Initiative connects real-time gross settlement systems of the countries in the GCC

Banks must evolve to compete in the Middle East market. Banks can remain relevant by digitizing customer journeys, acquiring or investing in fintechs, launching new products such as e-wallets and building an ecosystem, partnering with established ecosystem players or conglomerates, or carving out a stand-alone payments business from their active payments arm to act like fintechs to compete like other players in the space. Banks need to develop strategies to prepare for the implementation of open banking and the risk of disintermediation. Partnering with fintechs in the space on products in a similar nature to Goldman’s partnership with Apple and their launch of Apple Card can be a way to flourish in the open banking environment. Targeting the right segments will be imperative to incumbent banks’ success moving forward.

The Middle East as a target for consolidation among regional providers through M&A. Global players looking to capitalize on growth opportunities in the Middle East are expected to be seeking market share by targeting regional firms with local solutions accepted by the market. The Middle East is also attractive as a gateway to Africa’s payments market.