Buy Now Pay Later vs Credit Card

Written By: Ryo Hashimoto

Reviewed by: Ralph DiFiore (CCO), Marcus Magarian, Chris Gioffre

Americans’ personal expenditure appears to increase substantially during holiday seasons. Take Christmas for example, during America’s favorite holiday Americans spend hundreds, perhaps even thousands of dollars to finance their holiday expenses. In recent years, more and more Christmas shopping started to take place online. As the competition arises, online merchants are bending over backward to attract more shoppers. As one of the strategies, online merchants started to provide customers with more check-out options – we are not talking about accepting more credit card brands, but whole new payment options. Among them, “buy now, pay later,” or BNPL programs are having a resurgence in popularity.

In recent months, retail giants like Amazon, Airbnb, and Walmart have announced new partnerships with BNPL firms like Afterpay, Affirm Klarna, and Seezle giving shoppers the point-of-sale option of splitting the cost of purchases into equal installment payments spaced out over a predetermined period of time often, without interest. They are essentially a new form of layaway, except shoppers get the product before paying it off without putting down an upfront fee.

According to the research conducted by Credit Karma, 44% of respondents in the United States have used BNPL at least once to make a purchase as of September 2021.[1] Surprisingly, 38% of BNPL users think BNPL services will eventually replace their credit cards, and more than half (56%) answered that they prefer BNPL compared to using credit cards for purchases according to the survey conducted by C+R Research.[2]

So, the question now is why are BNPLs seemingly growing in popularity, and are they better than credit cards?

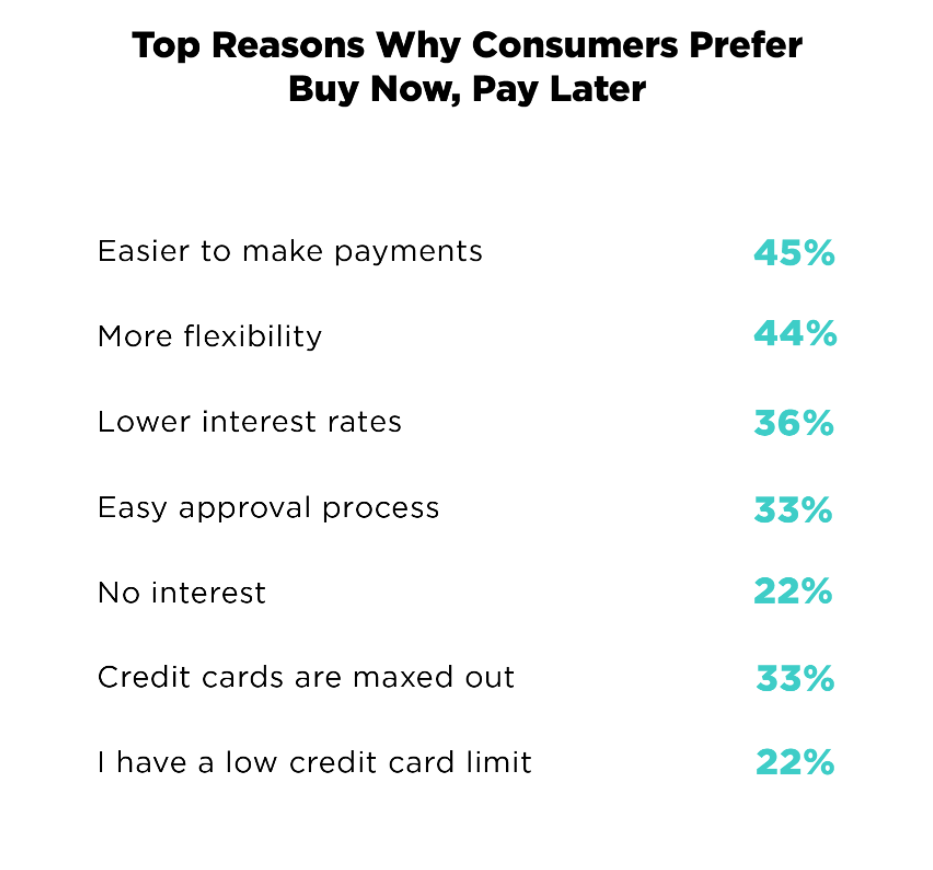

Why are BNPLs getting popular?

According to the survey carried out by C+R Research, one of the biggest draws of BNPL seem to be their simplicity and flexibility. Most BNPL services have either a fixed cost or no cost and are very upfront about showing you how much it will cost. I should say they are more straightforward compare to spending ten minutes reading through a ten-page credit card’s terms and conditions trying to figure out the interest payment. If you have a credit card, you have to pay at least the minimum payment at the end of the month, but with BNPL, you might have a three-, five- or 12-month option. You can set up the payment in different ways that work for you. Furthermore, for most BNPLs, all the payments take place on the mobile app which allows users to complete everything with the stroke of a key. Also, most BNPLs do not require any credit check and therefore, the buyers most likely get instantaneous approval. Simple and flexible payment structure and easy access clearly set BNPL apart from other payment options and make it an attractive way to shop.

Cost of Convenience

Well so, what is the cost? A lot of people have a perception where a massive “convenience fee” would creep up on you without you even realizing it when using such services. To my surprise, fees are not that terrible due to BNPL’s unique revenue model – merchants pay a fee to the platform they partner with to offer the service and then count on offsetting that cost by enticing shoppers to spend more than they would if they had to pay all at once. Thanks to the unique fee structure, the “fees” tend to be relatively low compared to credit cards. BNPL interest rates and fees vary widely. Some options carry no interest or fees at all, which essentially makes it free financing for the consumer. (BNPL providers still make money on the merchant fees baked into the price of the product, much like payment networks do on interchange fees for credit cards.) According to the Federal Reserve’s data for the third quarter of 2020, the average APR across all credit card accounts was 14.54%.[3] Simply looking at the interest rates, BNPL seems to have an advantage.

Downsides of BNPL

The whole point of having alternative payment methods online is to promote people to spend more money that most likely does not exist in their bank account. Although the “install payments” might make it look less evident this means consumers are actually taking on a loan. Borrowing money has a strong correlation with low financial well-being. Particularly, younger people are susceptible to the risks of opting into BNPL plans. Credit Karma reports that more than half of the Gen Z and millennial respondents said they had missed at least one BNPL payment, compared to 22% of Gen X and just 10% of Boomers.[1] This makes sense when you consider that many of these platforms appear to be specifically targeting younger shoppers. This indicates that BNPL has a greater potential impact on the younger generation with little financial literacy and disturbs their spending habits. This problem is not something that did not exist in the past: I bet a fair amount of people have experienced the horror of falling into credit card debt. However, it is certainly true that BNPL is adding to this issue by offering more accessible and flexible ways to make purchases.

So Credit Card or BNPL?

So going back to the original question, are BNPL products better than credit cards? Although, it seems like BNPL products might be a better deal than credit cards, it depends on the duration of payments. As long as you do not fall behind on scheduled payments, they are flexible and amounts are clearly stated upon the purchase. Is there anything that BNPL does not offer but a credit card does? Of course, there are. When you use a credit card to make purchases, you can earn cash back, points, or miles. If you have good credit, you can find a card that gives you at least 2% back on every purchase, which can add up to big savings. Credit cards also generally come with other benefits, such as purchase protection and insurance. BNPL providers don’t offer these kinds of rewards or protections, nor do they always offer the credit-reporting benefits of credit cards. Clearly, if you can pay the bills on time, then you are better off using credit cards. However, if you require a longer period of time to pay off the bill then, the lower interest rates that BNPL offers are hard to beat. Especially considering a lot of them offer no interest at all. After all, it is impossible to decide one way the or the other without looking to the conditions of each – duration of payments and interest rates play imperative roles in deciding which option saves more money. However, I am not surprised if BNPL appears to be the better option for a solid number of cases. I expect the BNPL will continue to attract shoppers and develops its unique market space.

Sources:

[1] “Buy now pay later surges throughout pandemic, consumers’ credit takes a hit” https://www.creditkarma.com/about/commentary/buy-now-pay-later-surges-throughout-pandemic-consumers-credit-takes-a-hit. Accessed 25 November 2021.

[2] “BUY NOW, PAY LATER STATISTICS AND USER HABITS” https://www.crresearch.com/blog/buy_now_pay_later_statistics. Accessed 25 November 2021.

[3] “Consumer Credit-G.19” https://www.federalreserve.gov/releases/g19/HIST/cc_hist_tc_levels.html. Accessed 25 November 2021.