Fintech and Covid – Tailwinds for Payment Platforms

Written By: Ryo Hashimoto

Reviewed by: Ralph DiFiore (CCO), Marcus Magarian, Chris Gioffre

Ever since the computer was invented, parents have scolded their children to get off their screens. The COVID-19 pandemic forced most children to live in a world where life became heavily dependent on screens. Far from scolding their children, parents encouraged children to get on the computer to further their education. The pandemic has drastically changed the normality of life for all ages; it not only inflicted a severe impact on our everyday lives but the entire economy has felt the turbulent disruption created by this unprecedented pandemic. In the United States, the unemployment rate reached an astounding 14.8% in April 2020[1], which marked the highest reported figure following the WWII era. Equally important, Gross Domestic Product dropped 3.5% in 2020, the biggest dip since 1946[2].

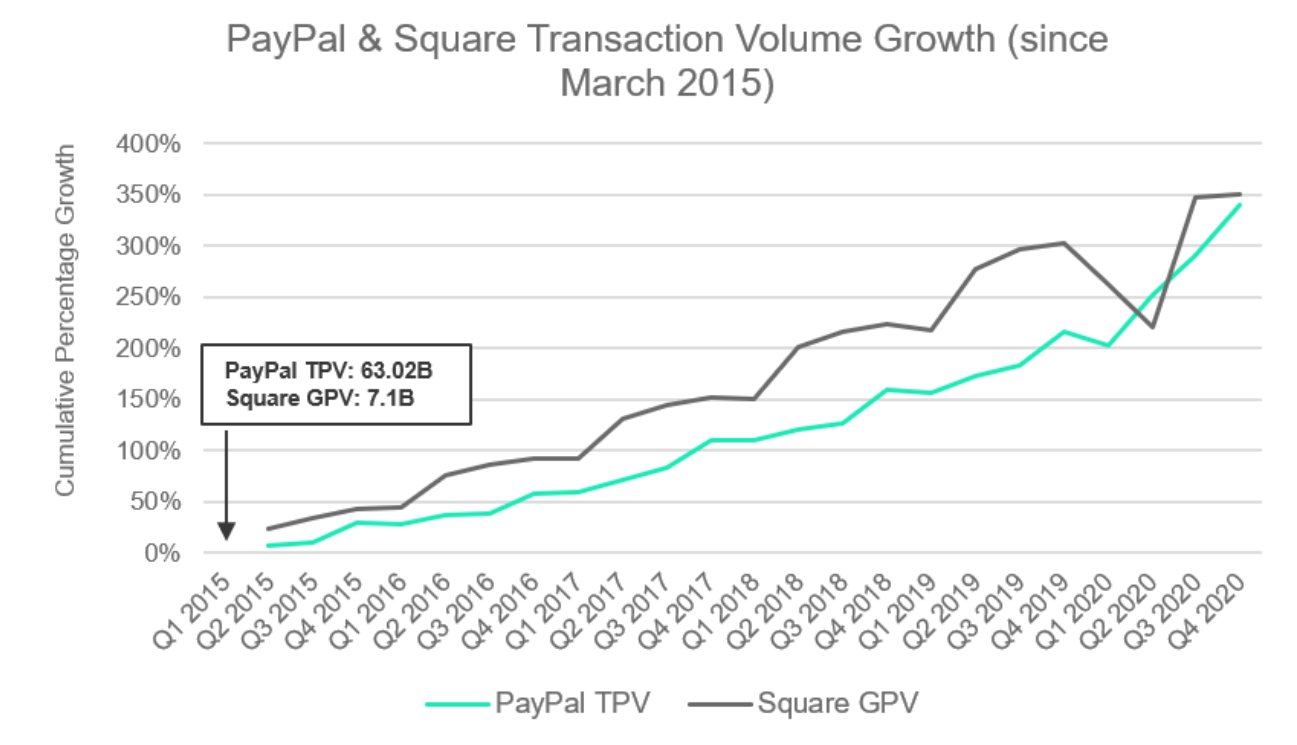

The fintech industry was impacted too – the pandemic continues to create substantial uncertainty for fintech companies that faced a number of challenges. Securing sufficient operating capital, keeping their workforce effective, or efficiently reducing the workforce were common challenges for a lot of fintech companies. However, some sectors within the fintech space have learned to convert pandemic-related hardship into business opportunities. In particular, some payment services have enjoyed significant tailwinds over the course of the pandemic. This includes Business to Customer (B2C) payments companies and Peer to Peer (P2P) companies. Both B2C (such as Square) and P2P providers (such as Venmo, CashApp) have seen strong growth in demand during the pandemic. Supporting this significant growth was Venmo’s quarterly Total Payment Volume of record-high $44.3 billion which was up 61% year-over-year[3].

Venmo and CashApp give consumers the ability to send and receive payments between bank accounts, credit cards, and e-commerce vendors. During the pandemic, the direct deposit volume on CashApp tripled and customers moved to store more than $1.3 billion in aggregate balances on their app[4]. Those platforms are perceived as safe ways to transfer money while maintaining COVID-19 protocols. Additionally, the growth in the outstanding balance was supported by its ability to receive stimulus payments. The revenue reported by PayPal, which owns Venmo, grew to $5.46 billion in the third quarter of 2020 up 25% from the same quarter one year earlier[4].

Square is mainly used by vendors to accept e-commerce and mobile payments. Venmo and Square focus on making the payment process as easy as possible for startups and small businesses. In addition to the conventional payment functionality, they expanded their services to financial services. Square launched “Square Banking”[5], a suite of financial products purposefully built to help small business owners easily manage their cash flow and get more out of their hard-earned money. By offering essential banking tools that work seamlessly within Square’s ecosystem of solutions, like payments and Square Payroll, sellers now have a single home for their entire business. This allows sellers to gain a unified view of their payments, account balances, expenditures, and financing options.

As a result of the pandemic, we had no choice but to rely more on digital technology. The payment services benefitted from the adoption of the “new normal.” While we are seeing the light at the end of the long pandemic tunnel, it will not stop those payment providers from innovating, and increased functionality will continue to attract more clients and potentially replace the traditional financial institutions.

[1] ”National Employment Monthly Update”: https://www.ncsl.org/research/labor-and-employment/national-employment-monthly-update.aspx

[2] “Gross Domestic Product, 4th Quarter and Year 2020 (Advance Estimate)”:

https://www.bea.gov/news/2021/gross-domestic-product-4th-quarter-and-year-2020-advance-estimate

[3] “PayPal’s pandemic winning streak continues; Venmo reaches $44 billion in volume”:

[4] “Disruptive Fintech during the Covid 19 pandemic”

[5] ”Introducing Square Banking, a Suite of Powerful Financial Tools for Small Businesses”