Payments in the Middle East

Author: Andrew Woolston (Intern)

Reviewed by: Ralph DiFiore (CCO), Marcus Magarian, Chris Gioffre

Consistent with the rest of the world, COVID-19 accelerated the adoption of digitized and contactless payments in the Middle East.

Despite 80-90% smartphone penetration in GCC Arab States, Israel, Iran, and other leading markets, the Middle East is still heavily dependent on cash. In the region, only one-third of retail transactions are conducted electronically. Underdeveloped digital-payments infrastructure and services, underbanked consumer and merchant segments, and a cultural preference for cash contributions to lacking digital payments integration.

In spite of this preference for cash, transactions card payments still managed to grow 70% in the year before the pandemic from February 2019 to January 2020. Another indication that sentiment is changing was found in the UAE where consumer digital payments transactions grew more than 9% annually between 2014 and 2019 (compared to Europe’s 4-5%).

Key Growth Statistics

- Saudi Arabia’s digital POS transactions doubled over 2020. 90% of survey participants believe more than half of new users will stick to digital solutions adopted during the pandemic.

- In McKinsey’s August 2021 survey on payments in the Middle East, more than 80% of respondents believed the growth rate of non-cash payments rose more than 10%. 43% placed the growth rate at over 20%.

With survey respondents favoring marketplaces and specialist fintechs over banks, local acquires, and e-wallets by 33% percent, respectively, SMEs are believed to seek solutions that go beyond pure payments. The growth opportunity resulting from SME preferences led 43% of respondents to believe that more than half of small and medium-sized merchants will start selling online in the next five years consequently resulting in growth in digital payments. In addition, lower merchant discount rates are expected to fuel the transition and adoption of digital payments.

Current Payments Sentiment in the Middle East

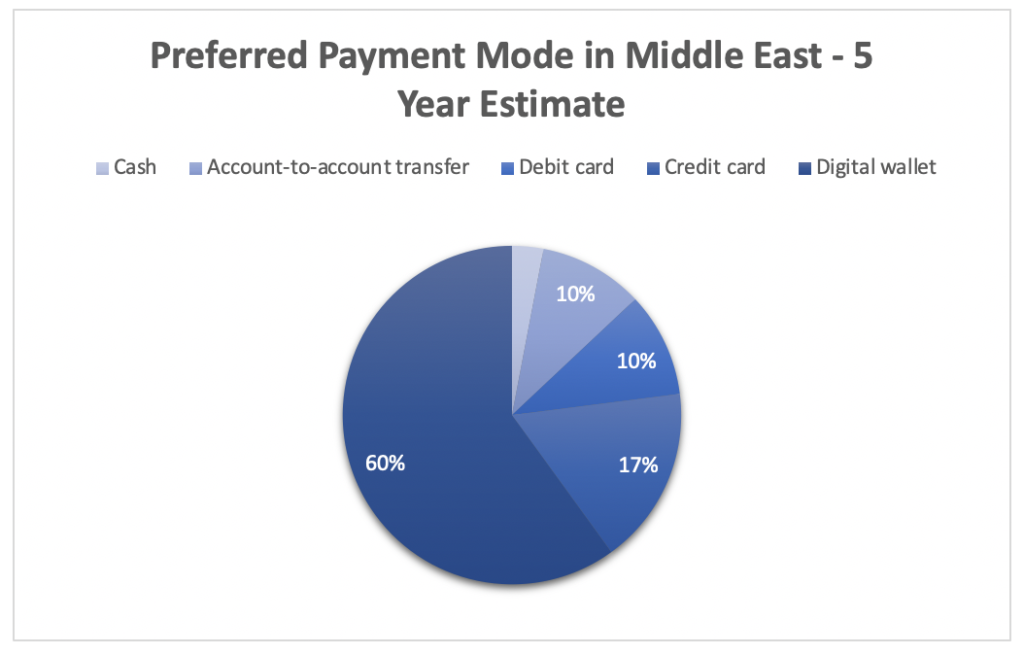

Despite COVID-19’s immediate impact, consumer preferences data supports the continued growth of the digital payments market in the Middle East. 58% of consumers in the Middle East expressed a strong preference for digital payment solutions.[1] Alternatively, only 10% strongly preferred cash. In the next five years, Middle East experts expect digital wallets (e-wallets) to be the most preferred mode of payment. The graph below depicts a five-year estimate of preferred payment methods in the Middle East based on the McKinsey survey mentioned above.

Nonbanks as Market Leaders

Global big-tech companies are expected to dominate consumer digital payments, with telecom company wallets and banks or bank-backed wallets trailing closely behind. In the Middle East, big-tech and telecom companies are favored in payments over incumbent banks due to their competitive advantage in technology expertise and well-established broad reach. These firms are expected to have a leg up in development and a better understanding of consumer preferences.

Telecoms’ success in digital payments.

Saudi Telecom Company’s STC Pay leveraged its strong telecoms presence to scale 4.5 million active customers by November 2020. 55% of mobile subscribers to STC Pay are STC customers. Partnerships with Western Union (raised $200 million at a $1.3 billion valuation) and Mastercard have enabled the company to cater to customer preferences and win market share.

Open Banking

Open Banking regulatory reforms are expected to help shape the future of payments in the Middle East. Open banking requires banks, with the consent of their customers, to share customers’ financial data with other banks or authorized financial services providers. In the Middle East, Bahrain passed regulations to institute open banking rules in 2018, followed by governance and data sharing guidelines in 2020. In early 2022, Saudi Arabia plans to launch open banking. Survey respondents identified regulatory approval for open banking as the leading catalyst for widespread customer adoption of digital payments. Incentivizing the shift from cash to digital payments for customers trailed open banking as a catalyst for digital payment adoption by 7%.

Open banking allows payments to avoid banks in the monetary transactions. 80% of survey respondents believe the implementation of open banking regulations will spark decoupling of savings account balances and payments capabilities. In this open banking environment, customers are expected to favor payment services companies with a better customer experience than banks, which tend to lack user-friendly payments ecosystems. STC Pay and other nonbanks can be expected to continue to thrive and win market share as the payments space transforms with open banking legislation.

Cross-border Ecosystem Developments

Cross-border payments in the Middle East require real-time, reliable digital payment infrastructure. The UAE and Saudi Arabia are home to two of the world’s three largest remittance corridors, processing $78 billion in payments in 2020. The necessity for agreements between countries for real-time settlement and the scaling up of digital money-transfer operators are expected to drive cross-border transactions in the near to mid-term.

| Active Cross-Border Transaction Initiatives in the Middle East | ||

| Initiative | Who | Description |

| Project Aber | Saudi Arabia & the UAE | Initiative produced a common digital currency between Saudi Arabia and the UAE |

| The Buna Payment Platform | Members of the Arab Monetary Fund | Initiative supports multicurrent payments among the members of the Arab Monetary Fund |

| The AFQ System | Countries in the Gulf Cooperation Council (GCC) | Initiative connects real-time gross settlement systems of the countries in the GCC |

Source: McKinsey

Opportunities for Banks to Compete

Banks must evolve to compete in the Middle East market. Banks can remain relevant by digitizing customer journeys, acquiring or investing in fintechs, launching new products such as e-wallets and building an ecosystem, partnering with established ecosystem players or conglomerates, or carving out a stand-alone payments business from their active payments arm to act like fintechs to compete like other players in the space. Banks need to develop strategies to prepare for the implementation of open banking and the risk of disintermediation. Partnering with fintechs in the space on products in a similar nature to Goldman’s partnership with Apple and their launch of Apple Card can be a way to flourish in the open banking environment. Targeting the right segments will be imperative to incumbent banks’ success moving forward.

The Middle East as a target for consolidation among regional providers through M&A. Global players looking to capitalize on growth opportunities in the Middle East are expected to be seeking market share by targeting regional firms with local solutions accepted by the market. The Middle East is also attractive as a gateway to Africa’s payments market.

[1] https://www.mckinsey.com/industries/financial-services/our-insights/the-future-of-payments-in-the-middle-east